The Executive Blueprint for Balancing Collections Outsourcing, Brand Preservation, and Compliance

The challenge of modern risk management requires balancing customer care with strict financial recovery. Enterprise organizations face massive operational friction when managing past-due accounts internally. This friction often deteriorates client trust. Forward-thinking financial leaders recognize that optimizing collections outsourcing represents a critical strategic turning point. By deploying an advanced strategy for first-party collections, institutions can recover outstanding revenue while fully safeguarding customer relationships. Choosing between internal customer care teams and external debt recovery partners remains a critical choice for operational leaders. This choice shapes the entire lifecycle of consumer brand equity.

Difference between First-Party and Third-Party Recovery in Collections Outsourcing

Understanding the structural boundary between recovery strategies is essential for corporate vetting committees. First-party collections outsourcing serves as a direct extension of your internal team. Agents communicate under your corporate name, using your brand identity across all borrower touchpoints. This method maintains a seamless customer service experience. Consequently, consumers do not feel penalized or isolated by the outreach process.

Conversely, third-party recovery occurs when an enterprise assigns or sells past-due debt to an external agency. These agencies operate independently under their own brand names. This shift in operational visibility changes the psychology of the customer interaction. While third-party agencies excel at late-stage, high-risk recovery, the transition often severs the historical client relationship. Enterprise organizations must analyze debt profiles to determine where first-party collections can preserve value before a third-party handoff becomes necessary.

Protecting Brand Reputation through Collections Outsourcing: Why First-Party Outreach Safeguards Client Trust

Preserving customer relationships during delinquency requires specialized, empathetic communication strategies. Traditional outbound phone tactics often alienate consumers and drive high abandonment rates. When you leverage first-party collections outsourcing, you embed brand safety directly into your financial recovery infrastructure. Dedicated customer care agents utilize localized communication methods to transform difficult financial conversations into collaborative payment adjustments.

Furthermore, maintaining an uncompromised customer relationship requires a seamless digital-first approach. Consumers actively screen traditional collections outreach via automated smartphone filters, making legacy dialer systems increasingly ineffective. First-party agents mitigate this issue by using integrated omnichannel platforms. These systems connect with consumers via preferred channels like SMS and email. This continuous, trusted communication helps organizations avoid customer churn and secure long-term consumer loyalty.

McKinsey Data on Digital Recovery Dynamics

The empirical data from McKinsey & Company underscore the immediate need to transform traditional debt operations. According to McKinsey’s research on digital collections dynamics, traditional outbound outreach strategies show a significant mismatch with modern consumer interaction preferences:

-

- The Communication Disconnect: McKinsey’s consumer surveys reveal that lenders heavily prioritize traditional phone calls and physical letters, especially during late-stage delinquency. However, delinquent consumers express an overwhelming preference for receiving communications primarily through digital channels such as email and text messaging.

- The Payment Propensity Multiplier: McKinsey data show that the “digital-first” consumer segment is 12% more likely to make a payment when contacted via preferred digital channels during early-stage delinquency.

- Late-Stage Liquidation Lift: The impact is even more pronounced in late-stage delinquency, where the likelihood that a digital-first consumer will make a payment increases by 30% when contacted through their preferred digital channels.

- The Full-Payment Phenomenon: The overall proportion of past-due customers who pay their balances in full doubles when organizations deploy tailored digital outreach rather than legacy voice-only calling models.

-40%

Operational Cost

Achieved by integrating advanced debt recovery platforms utilizing automated account segmentation.

+10%

Total Recovery Value Lift

Simultaneous increase in total portfolio liquidation through precision-targeted customer routing frameworks.

Furthermore, McKinsey highlights that advanced collections systems using automated segmentation report a 40% reduction in operational costs alongside a 10% increase in total recovery values. These precise metrics prove that modern customer retention depends entirely on deploying flexible, digitally integrated recovery models.

Navigating CFPB Rules in Customer-Facing Operations

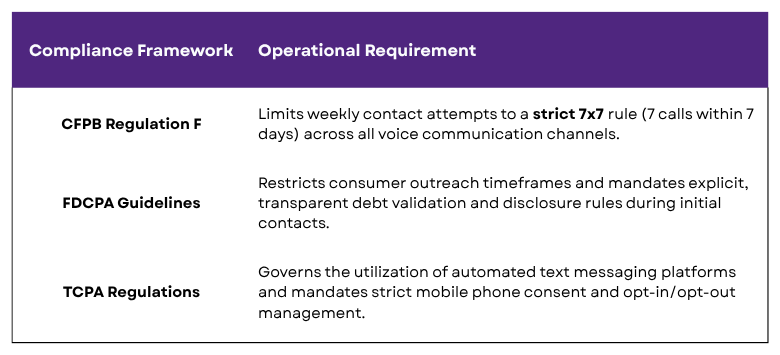

Operating a debt recovery infrastructure requires flawless alignment with federal consumer protection mandates. The Consumer Financial Protection Bureau (CFPB) enforces strict limits regarding consumer contact frequency and digital communication compliance. For instance, Regulation F implements rigid rules around the number of weekly call attempts allowed. Passing these limits triggers heavy regulatory penalties and creates systemic legal exposure for the parent corporation.

To eliminate compliance risk, enterprise organizations rely on collections outsourcing providers that integrate regulatory guardrails directly into their technology stacks. Automated contact centers prevent manual dialing mistakes by blocking outbound attempts once an account reaches daily or weekly communication thresholds. This systematic approach ensures that every customer touchpoint remains completely legal, auditable, and brand-safe.

Selecting the Right First-Party Collections Outsourcing Partner to Align with FDCPA Consumer Protections

Vetting an enterprise BPO customer service solution for a debt recovery partner requires checking their internal compliance architectures. A premier vendor must maintain verified compliance certificates, including SOC 2 Type II attestation and PCI DSS Level 1 compliance. These frameworks guarantee that sensitive customer financial data remains entirely secure across all digital environments.

Furthermore, leading BPO providers utilize advanced language tools to ensure consistent quality during live customer interactions. Our specialized tool, Accent Harmonizer, allows international agents to deliver exceptionally clear communication. This tech ensures that agents explain complex payment arrangements precisely and empathetically. Additionally, our intelligent workflow system, Arya, systematically analyzes accounts to match every consumer with their preferred communication channel. These capabilities allow enterprise organizations to scale their operations smoothly while lowering overhead and maximizing recovery performance.

The RCC Elevating Financial Performance and Operational Scale

Partnering with a trusted name for BPO customer service solutions for debt recovery offers immediate efficiency gains across your entire receivables portfolio. Our comprehensive collections outsourcing infrastructure replaces rigid, manual processes with real-time, data-driven workflows. By choosing our specialized first-party collections strategies, your organization secures a dominant market position while focusing on compliance and customer care.

Omnichannel Account Matching: Our automated systems analyze consumer behavior to route outreach to high-conversion channels such as SMS and email.

Proprietary Technology Deployment: We utilize our advanced Accent Harmonizer tool and Arya system to deliver exceptionally clear, personalized interactions that improve payment rates.

Certified Compliance Infrastructure: Our entire operation uses verified SOC 2 Type II, PCI DSS, and CFPB compliance engines to protect your enterprise from regulatory fines.

Strategic Brand Preservation: We act as a trusted extension of your business, resolving past-due balances under your name while protecting long-term client trust.

FAQ: First-Party & Third-Party Collections

What is the difference between first-party and third-party collections?

How does collections outsourcing protect our corporate brand reputation?

How do BPO customer service solutions for debt recovery maintain regulatory compliance?

What specific technology does RCC BPO use to optimize financial recovery?

Can first-party collections improve our overall customer retention metrics?

Capitalize on Enterprise-Grade Collections Outsourcing Solutions

Achieving optimal recovery performance requires a dedicated partner who understands how to blend regulatory precision with exceptional customer care. RCC BPO delivers elite BPO customer service solutions for debt recovery that help your brand lower high operational costs and eliminate compliance risks. Our specialized first-party collections infrastructure allows your business to optimize liquidation rates while consistently protecting consumer brand equity. Let our operations experts transform your collections outsourcing framework into a reliable engine for customer retention and revenue growth. Contact the RCC BPO partnership committee today to launch a comprehensive operational review of your portfolio.