How Lenders are Cutting Costs by 40% and Accelerating Growth with Dedicated Mortgage Outsourcing Services

What is Mortgage Outsourcing Service?

Mortgage Outsourcing are strategic partnerships where a financial institution—ranging from a commercial bank to a specialized non-bank lender—delegates specific, end-to-end components of the mortgage lifecycle to a professional Business Process Outsourcing (BPO) firm.

In 2026, this model has evolved from a simple back-office cost-cutting tool into a high-tech operational engine. The Global Mortgage Processing Outsourcing market is now valued at approximately $4.8 billion, growing at a CAGR of 8.5% as lenders prioritize agility over traditional fixed-staff models.

But what kind of capabilities do mortgage outsourcing services offer?

- Loan Origination Support: Precision in application intake and document collection.

- Mortgage Processing: Expert verification of employment, income, and title coordination.

- Underwriting Support: Data validation and condition clearing to ensure “ready-to-fund” files.

- Post-Closing & Quality Control: Rigorous document tracking and investor delivery.

- Loan Servicing Call Center Support: Managing the borrower relationship long after the keys are handed over.

The State of the Mortgage Market: Why the Status Quo is Failing

Current data from the Big 4 and industry leaders paints a stark picture for 2026. Non-bank lenders now outsource 42% of their operations to maintain liquidity. When production costs soar, the traditional “hire and fire” cycle of internal staffing becomes a strategic liability. This volatility leaves firms vulnerable to high overhead during volume dips. Today’s market leaders are no longer debating the merits of external partnerships. Instead, they are aggressively auditing how fast they can integrate mortgage outsourcing services to insulate their margins. By converting rigid, fixed operational burdens into variable, scalable engines, these agile competitors are outpacing those still clinging to legacy in-house structures.

The Strategic Benefits of Mortgage Outsourcing

To truly understand the benefits of mortgage outsourcing, one must look past simple labor arbitrage. The value lies in operational transformation and long-term resilience.

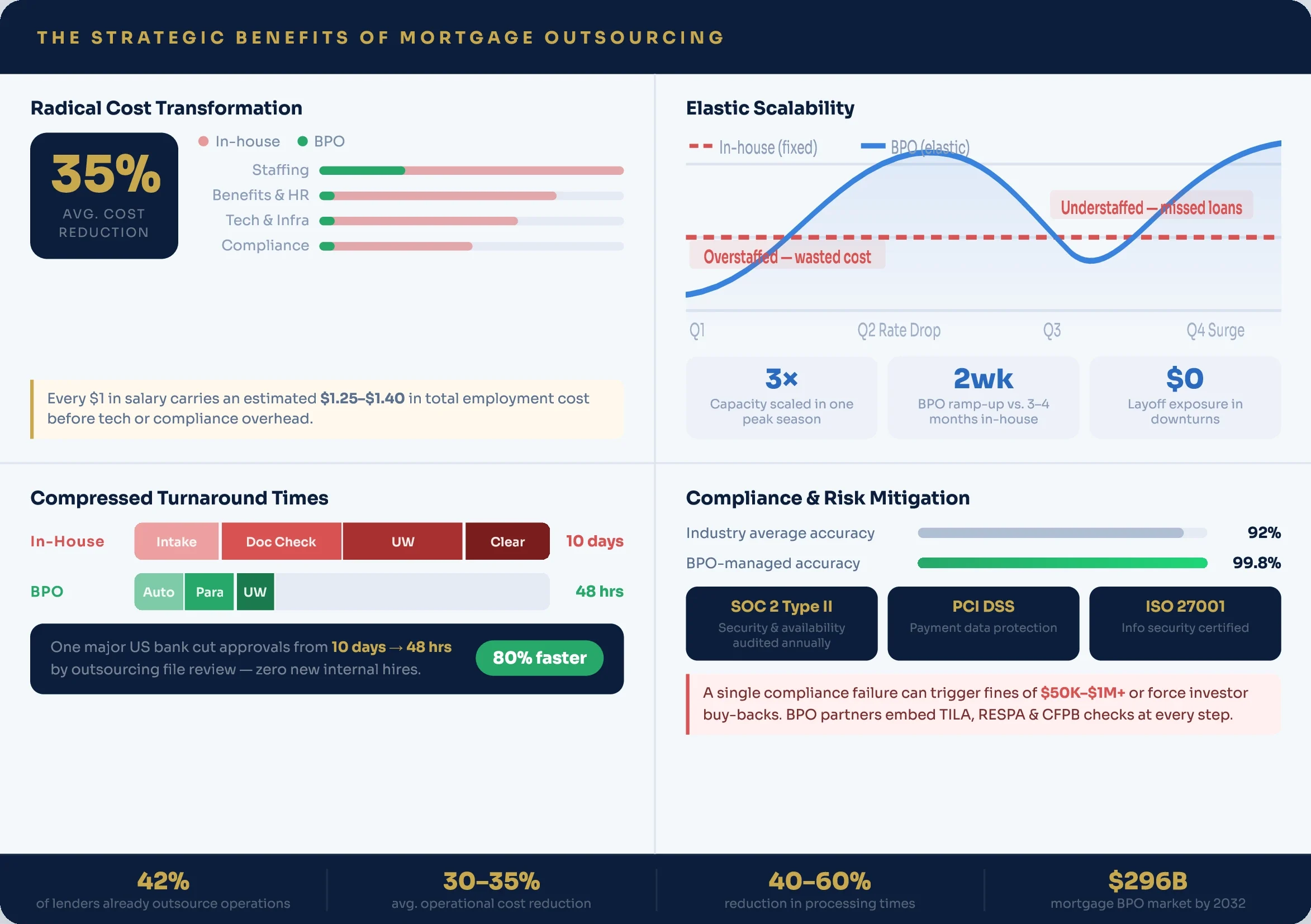

1. Radical Cost Transformation

- The Problem: Fixed internal salaries create massive “leakage” during low-volume months.

- The Solution: Mortgage outsourcing services transition your cost center to a “pay-per-loan” or “per-transaction” model.

- The Outcome: Lenders typically achieve a 30–35% reduction in operational costs, allowing them to reinvest capital into market expansion rather than overhead.

2. Compressed Turnaround Times

- The Problem: Manual document checks and “bottleneck” underwriting delay closings, frustrating borrowers and realtors.

- The Solution: BPO providers use automated workflows to handle repetitive data entry, freeing human experts to focus on complex decision-making.

- The Outcome: One major bank recently cut loan approval times from 10 days to just 48 hours by utilizing mortgage outsourcing services for file reviews.

3. Elastic Scalability

- The Problem: Scaling an in-house team to handle a sudden rate drop or seasonal spike takes months.

- The Solution: A specialized BPO partner maintains a “bench” of trained professionals ready to deploy immediately.

- The Outcome: Our partners can scale operations up or down within weeks, ensuring they never miss a peak or overpay during a trough.

4. Compliance and Risk Mitigation

- The Problem: Federal and state regulations are a moving target. A single compliance error can result in heavy fines or investor buy-backs.

- The Solution: Professional mortgage outsourcing services integrate compliance checks directly into the workflow and are backed by SOC 2 and PCI DSS standards.

- The Outcome: Regulators treat your BPO as an extension of your firm; having a partner with a 99.8% accuracy rate provides an essential safety net.

Mortgage Servicing Call Center Support: The Often-Overlooked Advantage for US Region

While many focus on the “front end,” the long-term profitability of a mortgage portfolio depends on loan servicing through the call center. After the loan closes, the borrower’s experience with payment queries, escrow analysis, and delinquency outreach determines your brand’s reputation.

Managing high-volume inquiries in-house is often cost-prohibitive. Specialized loan serving call center support ensures that every interaction is handled by agents trained in regulatory scripting and loss mitigation. This proactive outreach reduces delinquencies and improves CSAT scores. In a market where 51% of companies prioritize access to technology, a BPO provides the omnichannel infrastructure—chat, voice, and AI-driven help—that individual lenders often lack the CapEx to build.

Mortgage services do not exist in a vacuum. They are a critical component of the broader banking process outsourcing. For institutional lenders, integrating mortgage support with other BPO functions—such as AML/KYC monitoring, payments, and collections—creates a seamless operational ecosystem. Moreover, by viewing mortgage outsourcing services through the lens of banking process outsourcing, leadership teams can unify data across departments, leading to better risk assessment and a more holistic view of the customer.

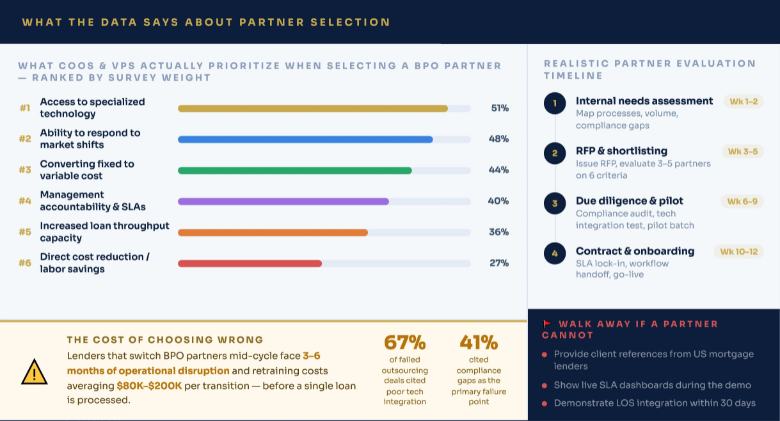

How to Choose the Right Mortgage Outsourcing Partner for US Region

Vetting a partner is a high-stakes decision for any COO or VP of CX. As you evaluate mortgage outsourcing services for US, ensure your shortlist meets these six strategic criteria:

- End-to-End Capability: Do they cover everything from application to mortgage servicing call center support?

- Proven Compliance: Can they demonstrate audit-ready trails for 2026 regulatory shifts?

- Technology Integration: Will their tech stack (like AI-driven document OCR) “talk” to your existing LOS?

- Variablez Pricing: Do they offer a true “utility” model that aligns with your volume?

- Specialized Talent: Are the agents mortgage-specific experts or generalist call center staff?

- Transparency: Do you have real-time visibility into SLAs and loan-level status?

Process-Driven FAQ: Mastering Mortgage BPO for USA

How do mortgage outsourcing services handle high-volume surges without sacrificing Quality Control (QC)?

We utilize an “Elastic Resource Bench” model. By integrating automated document indexing (OCR) with pre-trained mortgage processors, we maintain a 99.8% accuracy rate even when volume triples. Every file undergoes a secondary automated audit before being pushed back to the lender’s LOS, ensuring zero-defect delivery.

Can mortgage process outsourcing support the technical “Clear-to-Close” (CTC) phase?

Yes. Our teams specialize in the “heavy lifting” of the CTC phase. We handle final employment verifications (VOE), income refreshes (VOI), and also trailing document stacking. By outsourcing these administrative conditions, your senior in-house underwriters can focus exclusively on final credit decisions, effectively doubling your daily CTC throughput.

What is the fail-safe for regulatory changes within the mortgage loan servicing call center support?

Our compliance engine pushes real-time scripting updates to our loan servicing call center support teams. This ensures every agent is 100% aligned with the latest state and federal laws (such as CFPB updates or the Dodd-Frank Act) as soon as they go into effect, eliminating the risk of costly regulatory penalties during borrower interactions.

Does banking process outsourcing integrate directly with our existing Loan Origination System (LOS)?

Our banking process outsourcing infrastructure is API-agnostic. Whether you use Encompass, Blue Sage, or a proprietary system, our teams operate securely within your environment or via encrypted middleware. This ensures real-time pipeline visibility and zero data silos between your internal team and the BPO unit.

How does outsourcing resolve the “Trailing Document” bottleneck in the post-closing phase?

We deploy dedicated post-closing teams that proactively manage the chase for recorded mortgages and final title policies. By automating follow-up with title companies and local recorders, we reduce the time to deliver a complete, sale-ready loan package to secondary-market investors by up to 40%.