Evolving Digital Identity Verification in Banking Concerns Industry Experts on Australian Shores

Digital identity verification in Banking has transitioned from a back-office compliance task into a frontline strategic defense for Australian financial institutions. As we move toward 2026, the rise of synthetic identity fraud and sophisticated deepfakes has rendered traditional, document-heavy onboarding processes obsolete.

For decision-makers in Sydney, Melbourne and other major cities, the challenge is no longer just “checking a box” but building a digital verification system that stops fraud without destroying customer conversion. By implementing continuous identity assurance, banks can protect high-value assets while maintaining the seamless, low-friction experience that modern consumers demand.

Traditional Operational Inefficiencies in BFSI Fraud Prevention

The current Australian banking landscape reveals significant vulnerabilities in legacy identity frameworks. We have identified several critical gaps in current market offerings that increase operational risk:

- The “One-and-Done” Vulnerability: Most systems verify users only at onboarding. They fail to detect account takeovers that occur weeks or months later.

- Friction-Induced Abandonment: High-security hurdles often drive away legitimate customers. This directly impacts digital acquisition ROI and increases cost per acquisition.

- Siloed Intelligence: A lack of FRAML Integration creates blind spots. Fraud detection units and Anti-Money Laundering (AML) teams rarely share real-time data.

- Regulatory Desync: Many global systems overlook specific nuances in AUSTRAC and FMA reporting. This leads to compliance slippage and potential regulatory fines.

- Mobile-First Weakness: Legacy systems struggle with the Biometric Authentication capabilities built into modern smartphones. This creates a disjointed user experience.

Data Showing a Universal Shift to a Digital Verification System

According to the Deloitte 2024 Banking and Capital Markets Outlook, operational resilience and fraud mitigation are now top-tier board priorities. Furthermore, Gartner predicts that by 2026, the proliferation of AI-generated attacks will make Biometric Authentication an essential baseline for remote onboarding.

McKinsey & Company research highlights that leading institutions are shifting toward continuous identity assurance to counter the “industrialization of fraud.” These insights suggest that digital identity verification in banking must transition from static document checks to dynamic, behavior-based models. Leading firms in Australia are already moving toward FRAML Integration to unify their risk visibility.

Solving the Trust Gap via Behavioral Logic

- Behavioral Risk Profiling: Systems must monitor subtle user behaviors to flag anomalies before a fraudulent transaction is authorized.

- Localized Compliance Mastery: Every verification step must align with AUSTRAC requirements and the Australian Privacy Principles (APP).

- Unified Risk Visibility: Integration allows for faster decision-making. It reduces the operational overhead associated with investigating false positives.

- Step-Up Authentication: High-risk actions should trigger immediate biometric checks without interrupting low-risk, everyday banking support tasks.

When to Trigger Biometric Authentication and Decision Logic

Knowing when to apply friction is the hallmark of a sophisticated digital verification system. For instance, a digital identity verification in banking example would be a user attempting to change their linked mobile number from an unrecognized IP address. In this scenario, the system triggers a Biometric Authentication check.

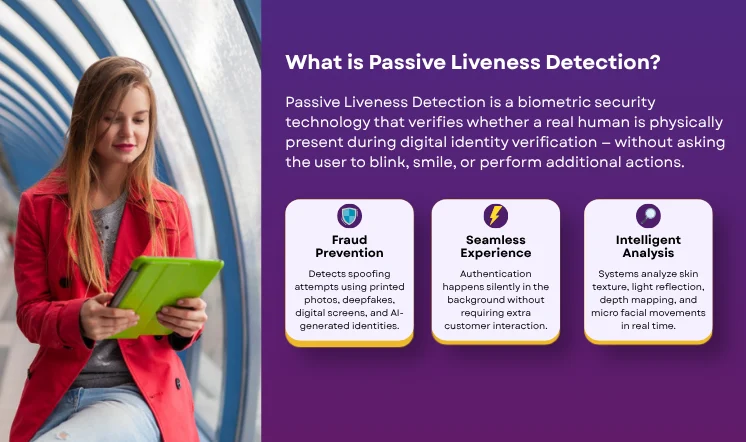

By using Passive Liveness Detection, the system analyzes micro-signals such as skin texture and light reflections to confirm human presence. This risk-based approach ensures that the majority of legitimate users experience zero delays. Meanwhile, high-risk activities face an immediate, robust defense. The goal is to move beyond “what you know” (passwords) to “who you are” (biometrics) and “how you act” (behavioral patterns). This multi-layered approach is the cornerstone of BFSI Fraud Prevention 2026.

Essential Technical Integration for Digital Identity Verification in Banking

Security is the absolute foundation of any modern financial service capability. As a SOC 2 compliant BPO, a provider must maintain the highest standards for data sovereignty and encryption. Our infrastructure supports BFSI fraud prevention 2026 goals by offering real-time audit trails. This speed is something legacy providers cannot match.

We focus on securing the entire customer lifecycle. This ensures that Digital Identity Verification in Banking remains a value-add rather than a bottleneck. By partnering with a specialist, your institution achieves both regulatory safety and competitive agility. Robust encryption and strict data handling ensure you remain compliant with the Consumer Data Right (CDR) in Australia.

Why Australian Banks Must Shift to Passive Liveness Detection Now?

The threat of “Presentation Attacks” using 3D masks or digital screens is rising in Australia. Passive Liveness Detection solves this by analyzing light reflection without asking the user to move. This technology is superior because it is invisible to the customer. It is, however, significantly harder for current AI tools to spoof. Implementing this today ensures your institution is prepared for the regulatory shifts expected by late 2025. It also reinforces your position as a security-first leader in the Pacific region.

The Future of Continuous Identity Assurance

The roadmap for 2026 involves moving away from periodic reviews. Instead, banks will adopt a model of continuous identity assurance. This means the identity is silently re-verified throughout the session. If a user’s navigation pattern suddenly changes, the system can pause the transaction. This level of protection is essential for high-net-worth accounts and corporate banking portals. It turns the digital verification system into a persistent guardian rather than a one-time gatekeeper.

In a concerted effort to curb fraudulent activity, Australia’s leading financial institutions—including Westpac, ANZ, CBA, NAB, Macquarie, and Suncorp—are rapidly integrating sophisticated artificial intelligence into their security protocols. This industry-wide shift prioritizes advanced identity verification methods such as biometric facial recognition via “selfies,” automated validation of government documents, and the monitoring of unique user behavioral patterns. By leveraging these high-tech tools, these major lenders aim to create a more robust defense against identity theft and unauthorized account access.

Frequently Asked Questions

-

How does digital identity verification specifically help with Australian compliance?

It automates the collection and verification of data required by AUSTRAC and the FMA. This ensures that your AML/CTF obligations are met consistently. It also removes the risk of human error in manual data entry.

-

What is the ROI on shifting to a behavior-based verification model?

Institutions typically see significant reductions in fraud losses and customer drop-off rates. By removing unnecessary “active” checks, you improve the conversion of your digital marketing spend.

-

Why is Passive Liveness Detection considered superior to active blinking tests?

Passive detection is much harder for modern generative AI to spoof. It also provides a better user experience because it happens in the background. It requires no extra effort or awkward movements from the customer.

-

How does a SOC 2 Compliant BPO protect our customer data in 2026?

A SOC 2 audit verifies that a provider has rigorous controls for data security and privacy. This reduces your third-party risk. It also ensures you remain compliant with the Consumer Data Right (CDR) and regional privacy laws.

-

Can this system be integrated with our existing banking core?

Yes, modern verification systems are designed for API-first integration. This allows you to add layers of biometric authentication and risk signals without a total overhaul of your legacy infrastructure.

Deploy Latest Digital Verification Systems with RCC BPO

The complexity of digital identity verification in banking requires a partner who understands the high stakes of the Australian financial landscape. We at RCC BPO invite you to vet these capabilities and see how a risk-first approach can optimize your customer onboarding and long-term security.

Schedule a call with experts at RCC BPO for a deep audit of current identity verification models and to identify areas for improvement.